E-Trade: An expensive, rigid brokerage

E-Trade: An expensive, rigid brokerage

Introduction

I had an E-Trade account to receive shares of stock from the company I worked for. But E-Trade’s behavior (from a user’s point of view) was far inferior to a typical self-serve brokerage service.

Working for a tech company, I had to sign up for an E-Trade account to receive stock awards and discounted stock purchases from the company. To be specific, I worked for the Canadian subsidiary of a USA-based company, and the account allowed me to receive restricted stock unit (RSU) grants which vested according to a schedule, and it allowed me to participate in an employee stock purchase plan (ESPP) to buy the company’s shares at a 15% discount.

At the same time, I had a (non-work-related) brokerage account at a Canadian bank in order to do my personal investment and stock trading activities. As of year , I found E-Trade to fall short of my expectations in a number of ways: High commission fees, restrictive transaction flow, and a busy user interface.

Summary of grievances

- $20 USD commission fee per sell order on stocks.

- Sell-to-cover for income tax withholding is a separate, involuntary order ($20).

- RSU shares vs. ESPP shares require separate orders ($20 each).

- Each user-initiated sell order must generate a cheque.

- But the cheque only contains the money from the transaction; it excludes the account cash balance from dividends and miscellaneous events.

- Website is complex and cluttered with non-useful tools and information. It makes selling stocks look complicated.

High transaction fees

First and foremost, E-Trade charges unusually high fees to process stock transactions. While brokerages in Canada charge a flat $10 CAD per trade and brokerages in the US charge under $10 USD (with the exchange rate roughly at par), E-Trade charges an exorbitant $20 USD per trade for international clients. (For employee stock plans, the only trade available is the sell order.)

To make matters worse, some trades are involuntary and the fees eat away at the income. Upon stock vesting, a portion of the stock is immediately sold to cover income taxes – at my marginal income tax rate of nearly 50%. Although E-Trade allows a few methods for the treatment of income taxes, my company chose the sell-to-cover method with no user override allowed. Alternative ideas include paying the withholding tax from personal cash (but this would be an uncomfortable spike at ~$4000 USD), or reconciling the tax difference later when filing the annual income tax return.

Unnecessary partitioning

There are two ways in which I receive stock in my E-Trade account:

RSU: The company promises me a block of stock shares over a period of time if I stay employed at the company. For example: A grant of 300 shares with 100 shares becoming vested on a specific date 1 year later, another 100 shares 2 years later, etc. This is effectively a form of extra income or a bonus.

ESPP: I spend part of my after-tax paycheck to buy the company stock at a 15% discount. The money is accumulated for a half year and the purchase is executed at the end of the period. Only the discount portion of the money (i.e. the fair market price minus the price I paid) is treated as additional income.

In the end, what I receive are shares of my company’s stock, regardless of whether it came from RSU or ESPP. But E-Trade begs to differ: It treats each of the two sources as different categories of stock, and I must place separate sell orders on each category, requiring a $20 transaction fee twice.

Compare this with my ordinary stock brokerage, where blocks of a particular stock bought at different times (or even transferred in from another account) all merge into a single mass of assets. Later when I perform a sell order, all the accumulated stock can be sold in one transaction costing only a single commission fee.

Restricted treatment of cash

An E-Trade employee stock account requires that after selling stock, the cash from the transaction is immediately dispensed to a cheque mailed to you. You cannot keep the cash proceeds in your account. This mostly makes sense because you can’t buy stock with the account or do anything else – except for one ugly little detail.

Some events generate cash that is kept in your account instead of being dispensed. Receiving dividends while holding onto stock is one example. Leftover change from a sell-to-cover transaction is another one (e.g. you sell 1 share at $60 to cover $40 of taxes, leaving $20 in change). You end up with a cash balance in your account, but you cannot merge the cash into the cheque dispensed after a sell order – you have to call E-Trade to explicitly dispense the cash. The workflow ends up being convoluted and suboptimal.

Delayed notifications

Upon an RSU vesting on a Wednesday, I received an email notification of the sell-to-cover-taxes transaction 2 business days later (Friday), and a notification of the vesting 4 days later (Tuesday). This is quite unacceptable, as my personal brokerage allows me to see orders in real time and events are posted to my online transaction log in real time. The time delay makes it harder to assess one’s financial position accurately and to make strategic trading decisions as soon as possible.

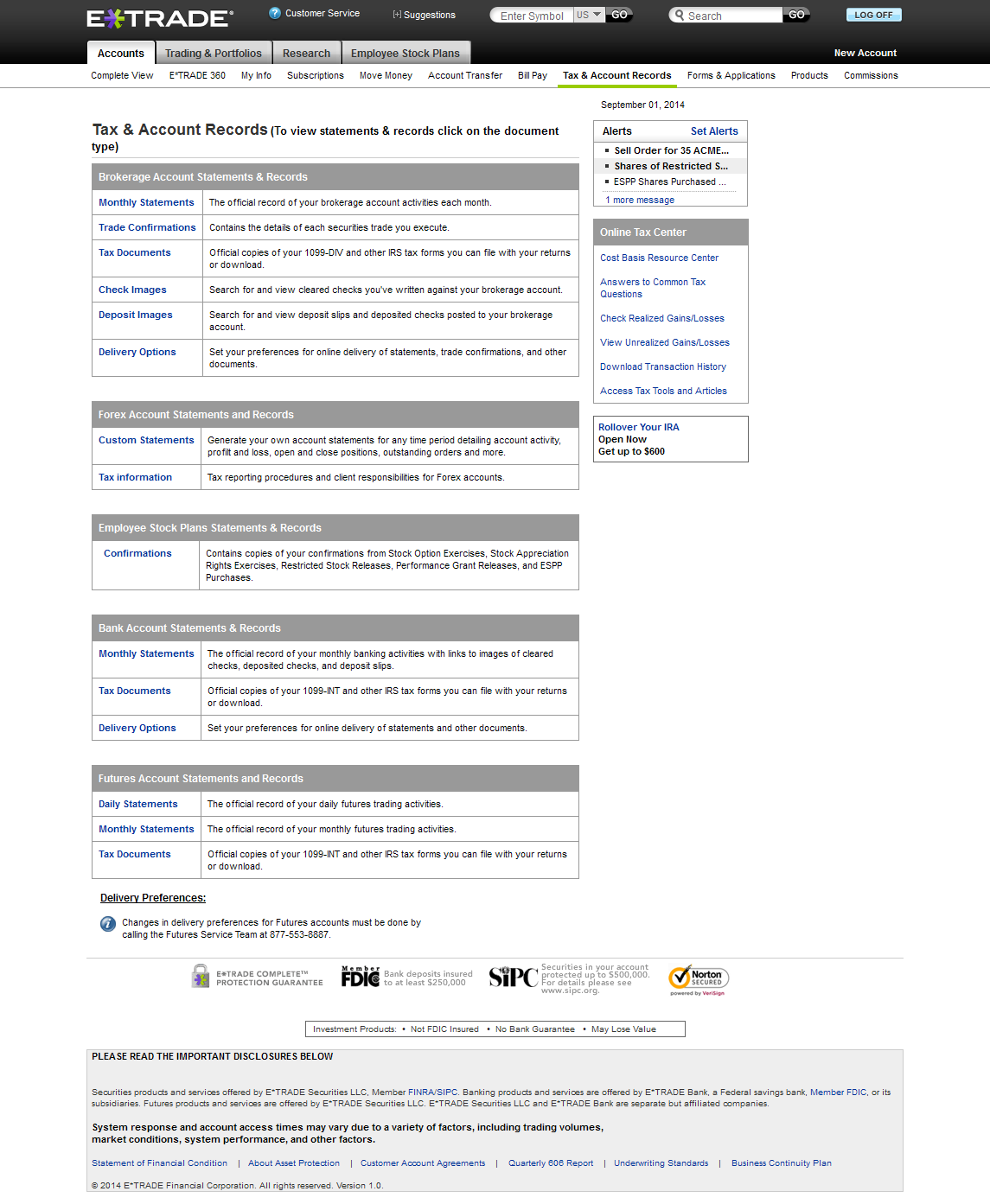

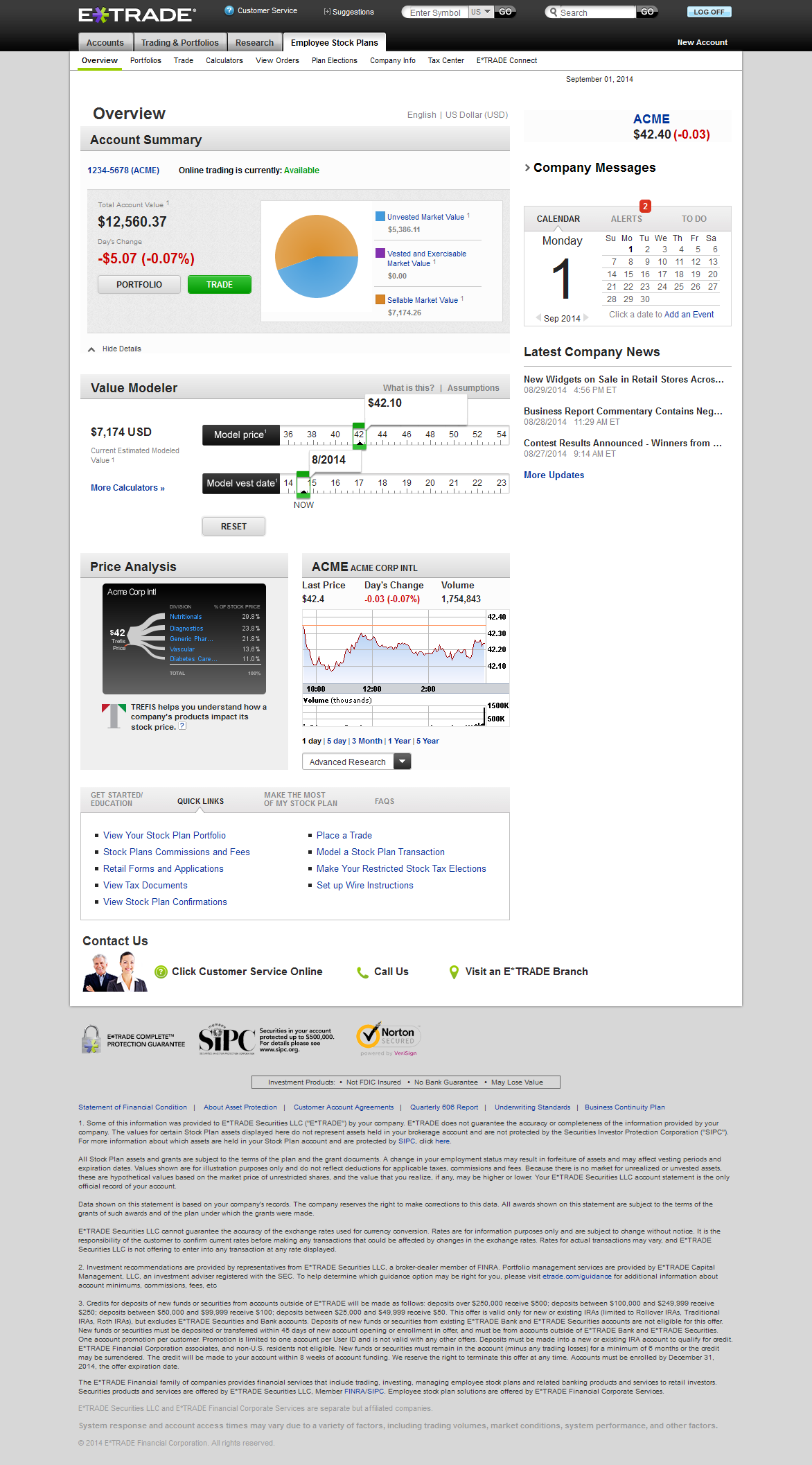

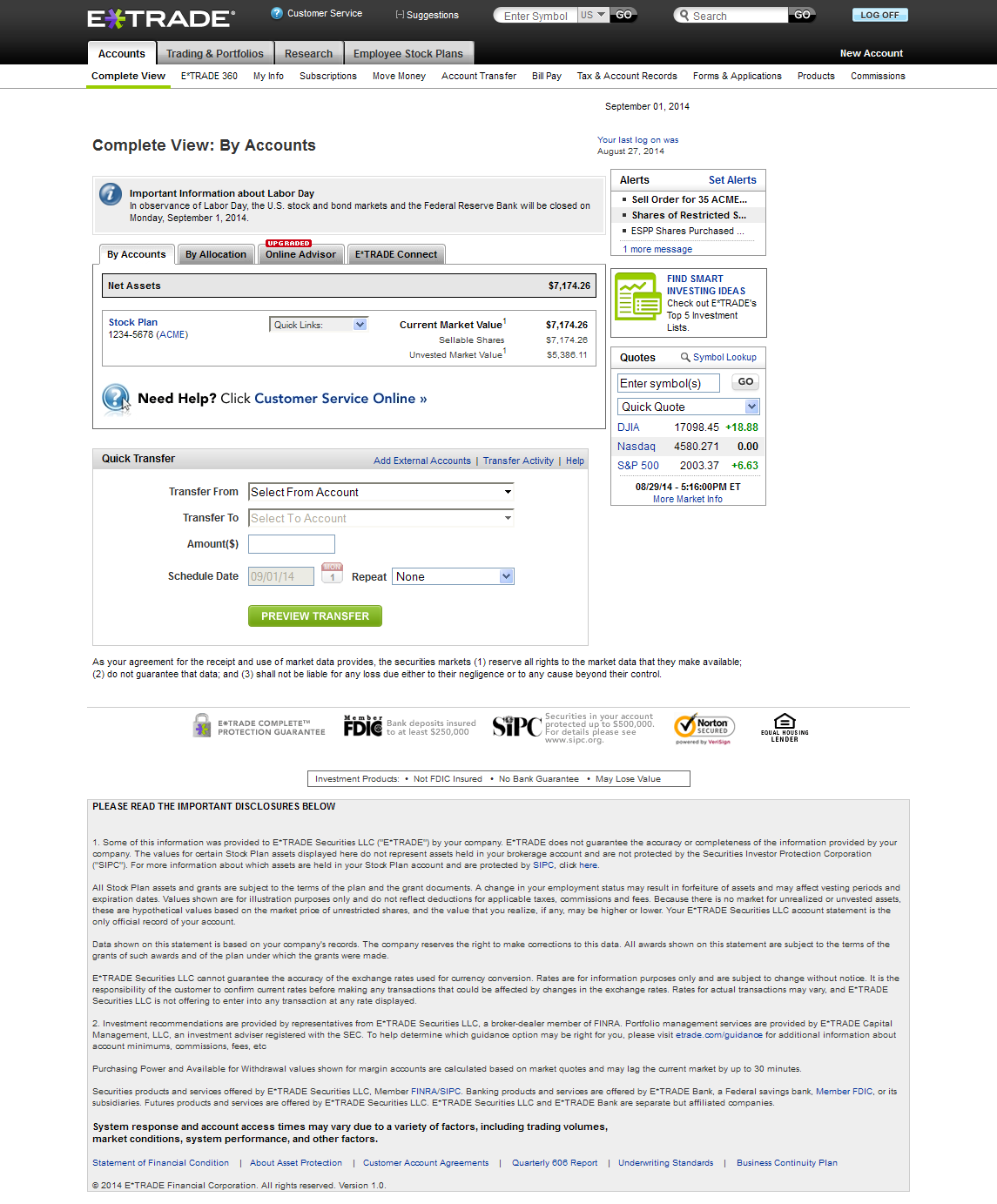

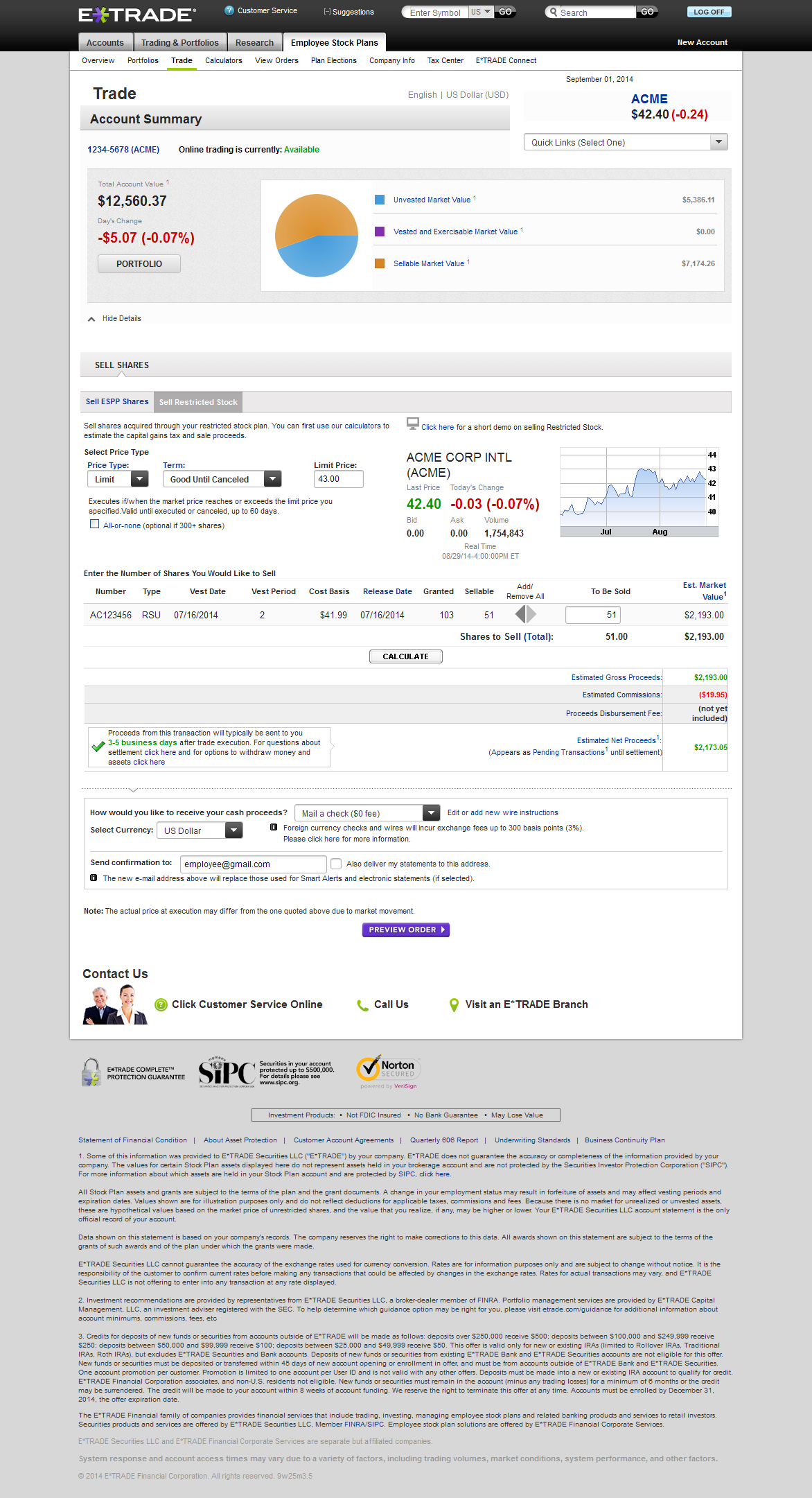

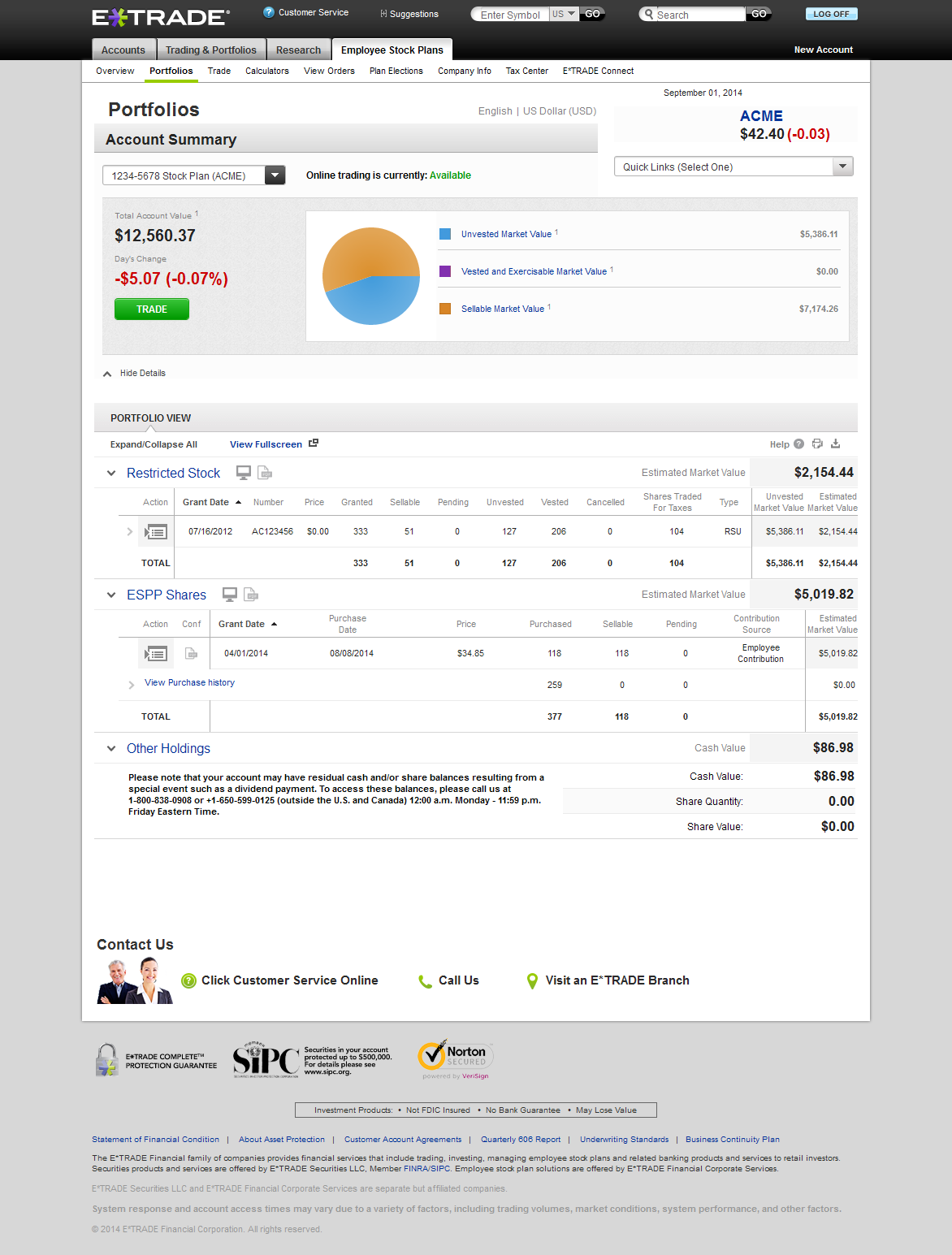

Cluttered website

What makes the user interface busy:

- Many sections and subsections in the top navigation bar

- Charts and monetary figures presented gratuitously

- Action links and boxes scattered everywhere

Picture examples of the web interface: